Key takeaways

- How AI enhances efficiency, accuracy, and customer satisfaction in the insurance industry.

- The role of AI in transforming risk assessment, claims processing, and customer service.

- The potential risks of AI in insurance, including data privacy, algorithmic bias, and the need for transparency.

Artificial intelligence (AI) is transforming numerous sectors, and insurance is no exception. Insurers have access to vast amounts of data, which AI can effectively leverage. By harnessing this data, insurance experts aim to enhance the efficiency and accuracy of customer service, fraud detection, underwriting and pricing, and sales operations using AI technology. The influence of AI in the insurance industry is growing, and we delve into some reasons behind this expansion below.

The AI in insurance landscape

The insurance industry thrives on risk management and future forecasting. As companies strive to meet regulatory standards and exceed consumer expectations, emerging technologies offer unparalleled advantages for those ready to innovate. Embracing these advancements can revolutionize predictive accuracy, transform customer interactions, and elevate personalized services and product offerings with unprecedented precision and efficiency.

The application of AI in insurance, so the question remains: how ready is the insurance sector to leverage these cutting-edge technologies to influence its future trajectory?

AI in insurance market size

AI is revolutionizing the insurance industry at an unprecedented pace. The global AI in insurance market, valued at $4.59 billion in 2022, is projected to skyrocket to an astounding $79.86 billion by 2032, according to Precedence Research.

This explosive growth underscores the game-changing impact AI is having on insurance. Forward-thinking insurers are leveraging AI to revolutionize claims processing, unearth fraudulent activities, personalize customer interactions, and dramatically improve the precision of policy underwriting. Despite the inherent complexities and steep learning curve of AI technologies, insurers are undeterred. They recognize AI's transformative power and are making bold investments to integrate it, ensuring they stay ahead in a rapidly evolving market.

The impact of AI in insurance

The rapid integration of AI in the insurance industry is revolutionizing the landscape, offering a myriad of transformative applications. From back office to front office operations, AI is set to redefine efficiency and accuracy. Imagine automating claims processing to deliver faster, error-free results, enhancing fraud detection to unprecedented levels, and streamlining agent and contact center activities for superior customer service. While human oversight remains a key component today, the horizon is bright with the promise of full automation, unlocking unparalleled potential and setting new standards for the industry.

Use case examples

AI's transformative power in the insurance industry is best illustrated through its diverse use cases. Let's look at some examples below:

Customer service

AI-powered chatbots and virtual assistants handle routine customer inquiries, provide instant responses, guide claims filing, and assist in purchasing policies. This automation offers 24/7 support, enhancing customer satisfaction and freeing human agents for complex issues. For example, a virtual assistant can help customers understand policy details or update personal information without human intervention.

Claims

AI in claims benefits both customers and insurance companies by shortening processing times and saving on payroll costs. Quick, accurate calculations lead to cost savings and provide agents with valuable recommendations. AI allows agents to focus on higher-skilled tasks by handling routine claims work. Additionally, AI-powered machine learning streamlines claims processing by analyzing images, sensors, and past data, enabling insurers to quickly review claims and predict potential costs.

Underwriting process

Traditional underwriting relies on historical data and manual assessments, which can be time-consuming and error-prone. AI can analyze a broader range of data sources in real-time, such as telematics from vehicles, health data from wearables, and satellite imagery. This leads to more accurate risk assessments and fairer premiums. For example, an AI system might adjust a driver's insurance premium based on real-time driving behavior data from a telematics device.

Fraud detection

AI technologies are capable of detecting anomalies in claims data and identifying incorrect information provided by customers with greater speed and efficiency than human capabilities. These tools can subsequently alert a claims specialist to investigate further.

Risk prevention

Leveraging sophisticated data analytics, AI enables insurance experts to swiftly analyze intricate datasets, such as historical claims records, customer demographics, market trends, and environmental data. AI aids in predictive modeling, evaluating loss data, and anticipating future risks. For example, AI can examine a client’s IoT data or claims history to offer insights into potential risk management challenges and the business’s overall risk tolerance. This information allows insurers to provide personalized guidance and proactively address problems before they result in substantial losses.

Personalized insurance products

By analysing customer data, AI can identify individual needs and preferences, allowing insurers to tailor their offerings accordingly. This level of personalization can lead to higher customer retention rates and increased loyalty. For example, an AI system might recommend additional coverage options based on a customer's lifestyle and risk profile, ensuring they have the most suitable protection. This not only enhances the customer experience but also helps insurers build stronger relationships with their clients.

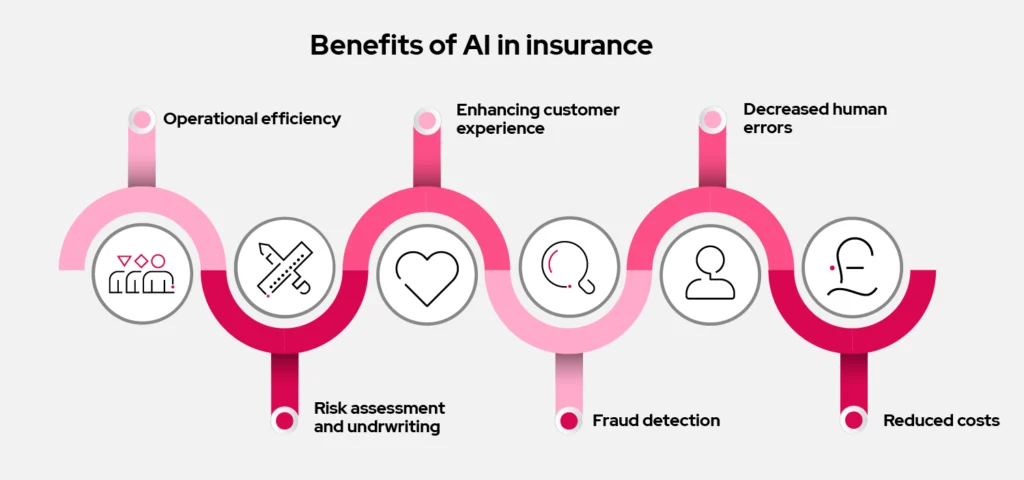

Benefits of AI in insurance

Integrating AI into the insurance sector can be a challenging endeavor, with many firms concerned about potential cybersecurity risks. The technology needs to prove its reliability and accuracy, especially for crucial applications. However, as the world and technology continue to evolve, the benefits of AI in insurance are becoming more apparent.

Here are some key advantages of incorporating AI in insurance agencies:

- Operational efficiency

- Risk assessment and undrwriting

- Enhancing customer experience

- Fraud detection

- Reduced costs

- Decreased human errors

Let's take a deeper look into each benefit.

Operational efficiency

AI-driven automation is revolutionizing the insurance industry by taking over mundane tasks like data entry, policy renewals, and claims processing. This allows human employees to concentrate on more intricate and rewarding activities. The result? Lower operational costs, faster service delivery, and happier customers.

Risk assessment and underwriting

Traditional methods rely on historical data and manual evaluations, which can be time-consuming and error-prone. AI can analyze vast data from sources like telematics, wearable devices, and satellite imagery in real-time. This enables more accurate risk assessments and pricing models, ensuring fairer premiums and reducing under or over-insuring.

Enhancing customer experience

AI-powered chatbots and virtual assistants offer 24/7 customer support, handling routine inquiries and guiding customers through processes like filing claims or purchasing policies. This ensures timely assistance and allows human agents to focus on complex issues. Additionally, AI personalises customer interactions by analysing preferences and behaviours, offering tailored recommendations and services. This personalisation can lead to higher customer retention and increased loyalty.

Fraud detection

Traditional fraud detection methods often rely on manual reviews, which can be slow and inefficient. Enter AI: a game-changer that can sift through massive datasets in real-time, spotting patterns and anomalies that might signal fraud. Imagine machine learning algorithms cross-referencing claims with historical data, instantly flagging anything suspicious for further investigation. This turbocharges the detection process and slashes the incidence of fraud, saving insurers a fortune.

Reduced costs

By leveraging AI, the cost of performing each task is significantly reduced due to accelerated processes. Additionally, employee satisfaction improves as they can concentrate on more engaging and less mundane tasks.

Decreased human errors

Traditionally, insurance interactions involved multiple parties and manual data input, increasing the risk of errors. AI tools can streamline processes, eliminate repetitive data entry, and ensure data consistency and accuracy.

Risks of AI in insurance

While AI offers numerous benefits to the insurance industry, it also presents several risks that insurers must carefully manage, such as:

- Data privacy and security

- Algorithmic bias

- Transparancy

Data privacy and security

AI systems depend on extensive data, including sensitive personal details, to operate efficiently. This reliance makes them appealing targets for cybercriminals. A security breach could jeopardize customer data, harm the insurer's reputation, and result in substantial financial losses. Consequently, insurers need to enforce strong cybersecurity protocols and adhere to data protection laws to protect their systems and customer information.

Algorithmic bias

AI algorithms trained on historical data may contain biases, leading to unfair treatment of certain customer groups, such as higher premiums for specific demographics. Insurers must regularly audit AI systems for bias and ensure diverse, representative data sets. Implementing an ethical AI framework is crucial for transparent, fair, and responsible AI operations.

Trancparancy

AI reliance can lead to a lack of transparency in decision-making, making it hard for customers to understand policy decisions and potentially eroding trust. Causal AI offers a more explainable form of AI, providing clear insights into decision processes. Insurers should aim for transparency, using Causal AI to explain decisions and maintaining open communication with customers.

The future of AI in insurance

As AI becomes more integrated into various sectors, it would be unwise and impractical to overlook its impact. The insurance sector typically operates in a conventional manner, but firms and their representatives must be ready to adapt swiftly to technological advancements to remain competitive and prosperous. Core insurance functions like claims, underwriting, and processing will persist, but the incorporation of AI in insurance aims to enhance the industry's efficiency, procedures, and overall productivity. To stay ahead of the curve, read more about future trends here.